The European Insurance and Occupational Pensions Authority (EIOPA) has published its information request on its proposed changes to Solvency II. This provides some insight into EIOPA's thinking following the consultation on its proposed changes to Solvency II (summarised in Milliman briefing notes here).

Interestingly, despite not proposing changes to the risk margin in its consultation papers, EIOPA is including a possible change to the risk margin in the impact assessment. The technical specification for the impact assessment sets out a scenario where the projected Solvency Capital Requirements (SCRs) used in the calculation of the risk margin are multiplied by a factor of 0.975 ("the lambda factor" ) compounded by the number of years between the valuation date and the projected date. This adjustment to projected SCRs is subject to a minimum of 50% (which bites at projection year 28). This tapering approach is mentioned in a paper by a working party of the Institute and Faculty of Actuaries that reviewed the risk margin and was included in a submission to EIOPA from the Association of British Insurers.

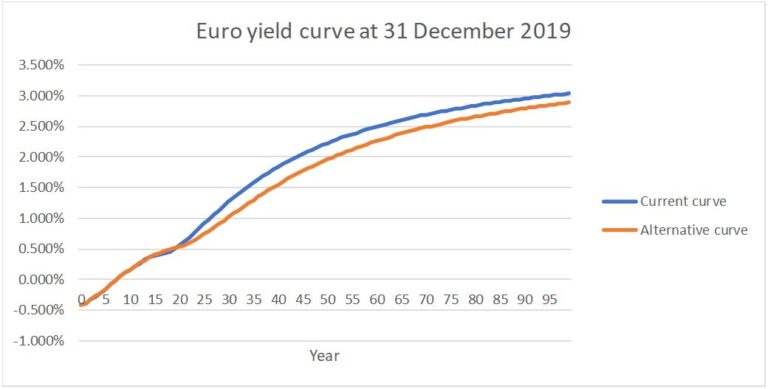

In relation to extrapolation, an alternative extrapolation method is proposed which affects the Euro yield curve at 31 December 2019 as shown in the graph below. This is one of the five options proposed in the EIOPA consultation paper.

As can be seen, the impact is to reduce the Euro curve after the Last Liquid Point (LLP), but not as materially as some of the other EIOPA proposals that were included in the consultation which involved increasing the LLP. Non-Euro yield curves will also be affected but less materially, as the LLP is later. By comparison the UK yield curve actually increases at later durations using this approach.

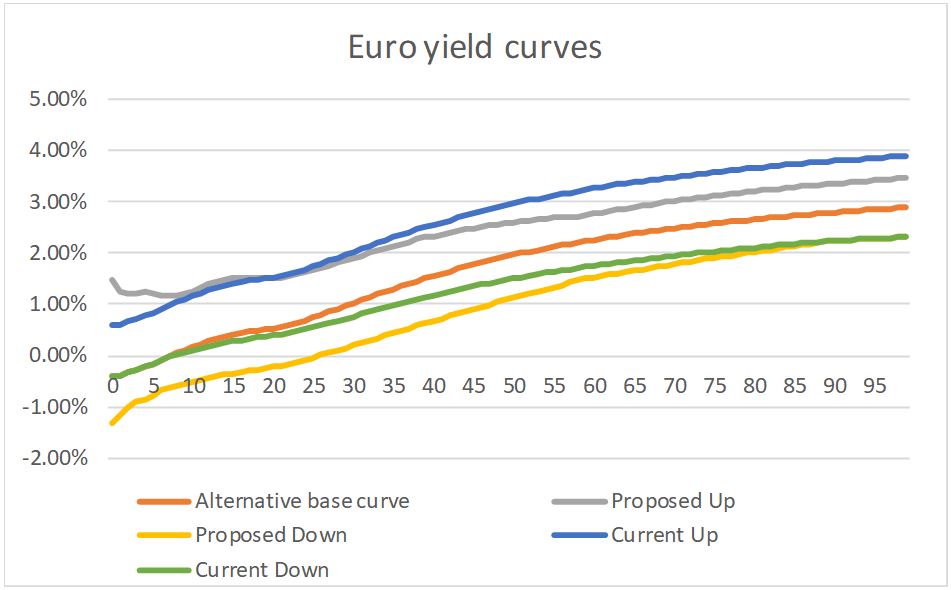

Unsurprisingly, interest rate shocks are proposed which increase the impact of the interest rate down shock for the Euro yield curve. The graph below shows the interest rate shocks that would apply as at 31 December 2019 using the current approach and those proposed in the impact assessment (both based on the alternative base Euro yield curve proposed above).

As can be seen, the proposed interest down shock would increase the impact of this shock (while the impact of the interest up shock would reduce).

Several other changes are being assessed, including:

- Reflecting realistic new business assumptions in best estimate expenses

- Correlation factor between interest rate risk and spread risk

- Volatility adjustment

- Dynamic volatility adjustment in standard formula (and internal models)

- A floor on the interest rate down shock

- Long-term equity requirements for use

- Recognition of risk mitigation techniques

- Non-life Minimum Capital Requirement factors

- Contract boundaries clarification

Supervisors have notified companies that are required to participate in the impact assessment. Submissions are due 31 March 2020. EIOPA's final opinion on the 2020 review of Solvency II is due in June.