The Milliman Mortgage Default Index (MMDI) is a lifetime default rate estimate calculated at the loan level for a portfolio of single-family mortgages. For the purposes of this index, default is defined as a loan that is expected to become 180 days or more delinquent over the life of the loan.1 The results of the MMDI reflect the most recent data acquisition available from Freddie Mac and Fannie Mae, with measurement dates starting from January 1, 2014.

Key findings

Interact with the MMDI

To explore the MMDI data on a more granular level, including loan origination and type, click here.

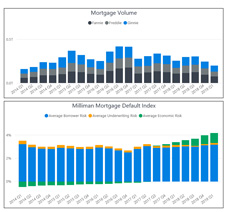

Interest rates continued to increase during the third quarter (Q3) of 2022, and this increase has had a large impact on the mortgage market. Mortgage originators have observed a large decrease in origination volume, particularly with mortgage refinances. Year over year, total mortgage acquisition volume is down 62% for Freddie Mac and Fannie Mae. Refinance activity is driving most of the decline and is down 87% year-to-date.

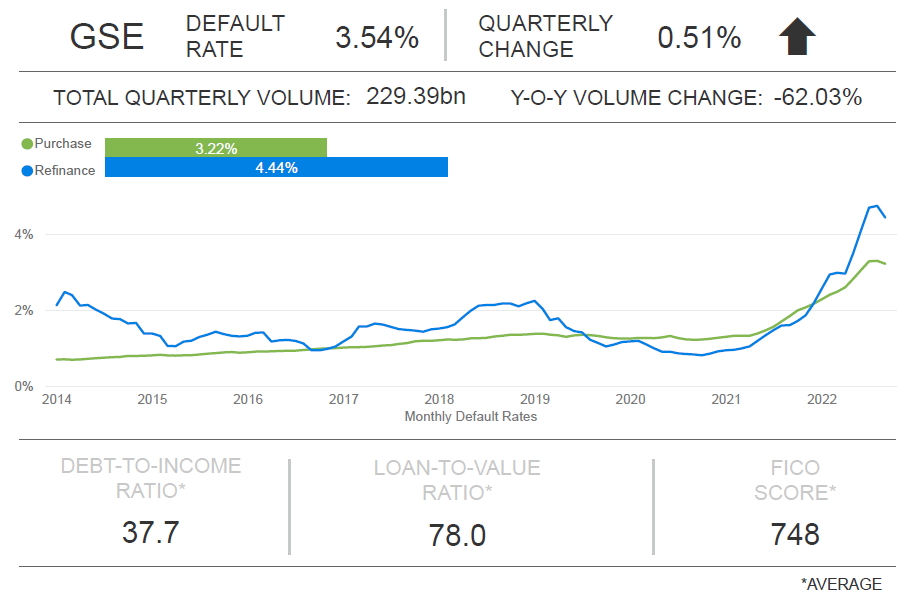

This large change in the composition of loans is having a similar impact on the default risk of originations. Generally, purchase mortgages have higher risk attributes relative to refinance loans. The index value of the MMDI was 3.54% for loans originating in 2022 Q3 compared to 3.02% for 2022 Q2 originations. Figure 1 provides the quarter-end index results, segmented by purchase and refinance. Another driver of increased default risk, for both purchase and refinance, is an expected slowdown of home price growth over the next several years.

Figure 1: MMDI 2022 Q3 dashboard for GSE loans

Summary of trends

Over 2022 Q3, our latest MMDI results show that mortgage risk increased for Freddie and Fannie acquisitions. There are three components of the MMDI: measures for borrower risk, underwriting risk, and economic risk. Borrower risk measures the risk of the loan defaulting due to borrower credit quality, initial equity position, and debt-to-income ratio. Underwriting risk measures the risk of the loan defaulting due to mortgage product features such as amortization type, occupancy status, and other factors. Economic risk measures the risk of the loan defaulting due to historical and forecasted economic conditions. In 2022 Q3, each of these risk measures were higher than in 2022 Q2.

BORROWER RISK RESULTS: 2022 Q3

For government-sponsored enterprise (GSE) loans, borrower risk increased from 1.57% in 2022 Q2 to 1.61% in 2022 Q3 with purchase loans making up about 80% of total originations compared to 62% last quarter. When compared to refinance loans, purchase loans are correlated with higher borrower risk as it is typical for the borrowers to have lower credit scores and higher loan-to-value ratios. Thus, an increase in borrower risk is expected.

UNDERWRITING RISK RESULTS: 2022 Q3

Underwriting risk represents additional risk adjustments for property and loan characteristics such as occupancy status, amortization type, documentation types, loan term, and others. Underwriting risk after the global financial crisis remains low and is negative for purchase mortgages, which were generally full-documentation, fully amortizing loans. For refinance loans, a greater portion of originations are cash-out refinance loans (as opposed to refinancing for more favorable rate and/or length-of-loan terms) given recent robust home price growth. Cash-out refinance loans are assigned a greater default risk and are contributing to increases in underwriting risk.

ECONOMIC RISK RESULTS: 2022 Q3

Economic risk is measured by looking at historical and forecasted home prices. For GSE loans, economic risk increased from 1.39% in 2022 Q2 to 1.91% in 2022 Q3. Actual home price appreciation has been robust from 2014 through 2022, which has resulted in embedded appreciation for older originations. This results in reduced default risk for older cohorts. For more recent cohorts, we anticipate slower home price growth (or negative growth for some local geographies), which contributes to increases in economic risk for recent origination years.

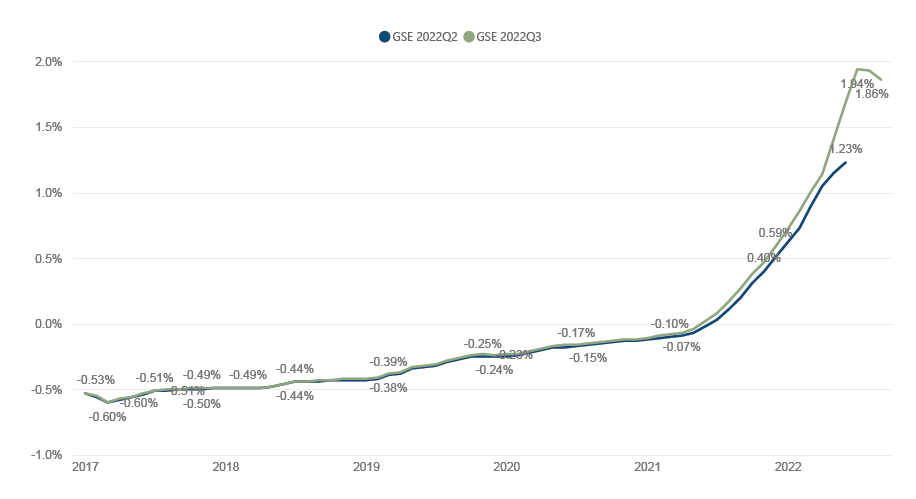

Figure 2 shows the economic risk component of the MMDI for GSE mortgages as of 2022 Q2 and 2022 Q3.

Figure 2: Economic risk by investor and origination

We notice from the chart that economic risk has remained steady for older originations, while economic risk for newer originations has sharply increased as we anticipate slower to negative home price growth in the future. For more information on the housing market, please refer to our recent Milliman Insight article, “The housing market is slowing down...what does that mean?” available at https://www.milliman.com/en/insight/housing-market-is-slowing-down-what-does-that-mean. This publication of the MMDI uses the most recent data available to provide timely information on credit trends.

The MMDI reflects a baseline forecast of future home prices. To the extent actual or baseline forecasts diverge from the current forecast, future publications of the MMDI will change accordingly.

About the Milliman Mortgage Default Index

Milliman is expert in analyzing complex data and building econometric models that are transparent, intuitive, and informative. We have used our expertise to assist multiple clients in developing econometric models for evaluating mortgage risk both at the point of sale and for seasoned mortgages.

The Milliman Mortgage Default Index (MMDI) uses econometric modeling to develop a dynamic model that is used by clients in multiple ways, including analyzing, monitoring, and ranking the credit quality of new production, allocating servicing sources, and developing underwriting guidelines and pricing. Because the MMDI produces a lifetime default rate estimate at the loan level, it is used by clients as a benchmarking tool in origination and servicing. The MMDI is constructed by combining three important components of mortgage risk: borrower credit quality, underwriting characteristics of the mortgage, and the economic environment presented to the mortgage. The MMDI uses a robust data set of over 30 million mortgage loans, which is updated frequently to ensure it maintains the highest level of accuracy.

Milliman is one of the largest independent consulting firms in the world and has pioneered strategies, tools, and solutions worldwide. We are recognized leaders in the markets we serve. Milliman insight reaches across global boundaries, offering specialized consulting services in mortgage banking, employee benefits, healthcare, life insurance and financial services, and property and casualty (P&C) insurance. Within these sectors, Milliman consultants serve a wide range of current and emerging markets. Clients know they can depend on us as industry experts, trusted advisers, and creative problem-solvers.

Milliman's Mortgage Practice in Milwaukee is dedicated to providing strategic, quantitative, and other consulting services to leading organizations in the mortgage banking industry. Past and current clients include many of the nation's largest banks, private mortgage guaranty insurers, financial guaranty insurers, institutional investors, and governmental organizations.

1 For example, if the MMDI is 10%, then we expect 10% of the mortgages originated in that month to become 180 days or more delinquent over their lifetimes.