{kind=link}

A well-funded pension plan implemented Milliman’s Segment Matching-Surplus Management (SM2) approach to liability-driven investing (LDI) at the beginning of 2011. Even though equities produced less than expected returns and corporate bond rates reached historic lows, this plan’s funded status remained stable in 2011, precisely as predicted.

Issue: After years of volatile annual contributions, the Investment Committee wanted to stabilize contributions and protect their pension plan’s funded status.

Due to additional contributions and favorable equity returns in 2009 and 2010, the plan was nearly 100% funded on an ongoing basis at the beginning of 2011. However, with 70% of their assets in equities, the investment committee knew that the plan was very susceptible to downturns in the market. The committee was also aware of the sensitivity of their plan’s liabilities to changes in the underlying discount rates. The client was comfortable with the prospect of slightly higher annual contributions as long as they remained stable for the purposes of budgeting and planning.

Solution: Execution of Milliman’s SM2 approach to LDI and Pension Performance Dashboard (PPD) monitoring tool.

In the “marked to market” environment brought on by the Pension Protection Act and FASB changes, the client wanted to focus on better matching movements in plan assets to movements in plan liabilities, since this difference is what will now influence the variability of contributions to the plan, The analysis phase included examination of contributions and funded ratios under multiple economic scenarios and asset allocations, as well as immediately shifting their current fixed income holdings to “PPA Smart” segment-matched fixed income until a course of action was prescribed.

Based on the analysis performed, the Investment Committee chose to implement Milliman’s SM2 strategy in early 2011. In conjunction with the implementation of SM2, the Pension Performance Dashboard would be used to monitor SM2’s effectiveness. The SM2 strategy included matching the plan’s liabilities occurring in Segment 1 (0-5 years) and Segment 2 (5-20 years) with two portfolios of bonds with durations similar to the liabilities (PPA Smart). Segment 3 (20+ years) liabilities were unmatched and the remaining assets were invested in a diversified equity portfolio of best-in-class managers.

Outcome: The Investment Committee’s decision to incorporate an LDI strategy resulted in an improvement in funded position of $15 million and a reduction of $2.6 million for the 2012 plan year minimum required contribution.

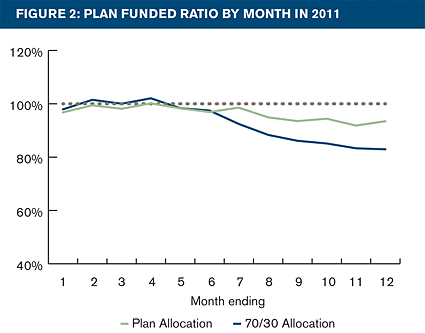

At the beginning of 2011, the plan had a funded ratio of 96%. Based on the plan’s SM2 allocation throughout 2011, the plan held $135 million in assets and reached a funded ratio of 93% as of December 31, 2011.

The reduction in the plan’s funded ratio from 96% to 93% under the SM2 approach was attributable to the equity portfolio, which was unmatched with the plan’s liabilities.

Figure 1 compares the asset and liability returns by segment for 2011. The Risk Fund, which represents the bond portfolios designed to match the plan’s liabilities in Segments 1 and 2, produced a funding surplus in 2011. The unmatched Return Fund, which reflects Segment 3 liabilities and assets invested in the equity portfolio, produced an offsetting funding shortfall in 2011.

If the plan had retained the old investment policy of 70% equities and 30% fixed income, the plan’s funded ratio would have decreased to 83% at year-end. In addition, the plan would have had a reduction of approximately $15 million in funded position as compared to the SM2 approach that the Investment Committee implemented.

Figure 2 compares the plan’s monthly funded ratio throughout 2011 under the plan’s SM2 allocation and the plan’s previous investment allocation of 70 percent equity and 30 percent fixed income.

As a result, the Investment Committee’s decision to incorporate SM2 reduced the company contribution due for 2012 by approximately $2.6 million.